The implementation of the Markets in Crypto-Assets (MiCA) regulation marks a turning point for the digital asset industry, shifting the ecosystem from a fragmented regulatory landscape toward a unified, high-trust environment. The French regulator has approved Triple-A (a Singapore-based stablecoin fintech company) as a Crypto-Asset Service Provider (CASP). This allows them to operate as a regulated counterparty across all 30 EU and EEA countries. This development highlights how international firms are adapting to EU standards to unlock the massive potential of a single, standardized market.

What does the MiCA framework mean for crypto service providers?

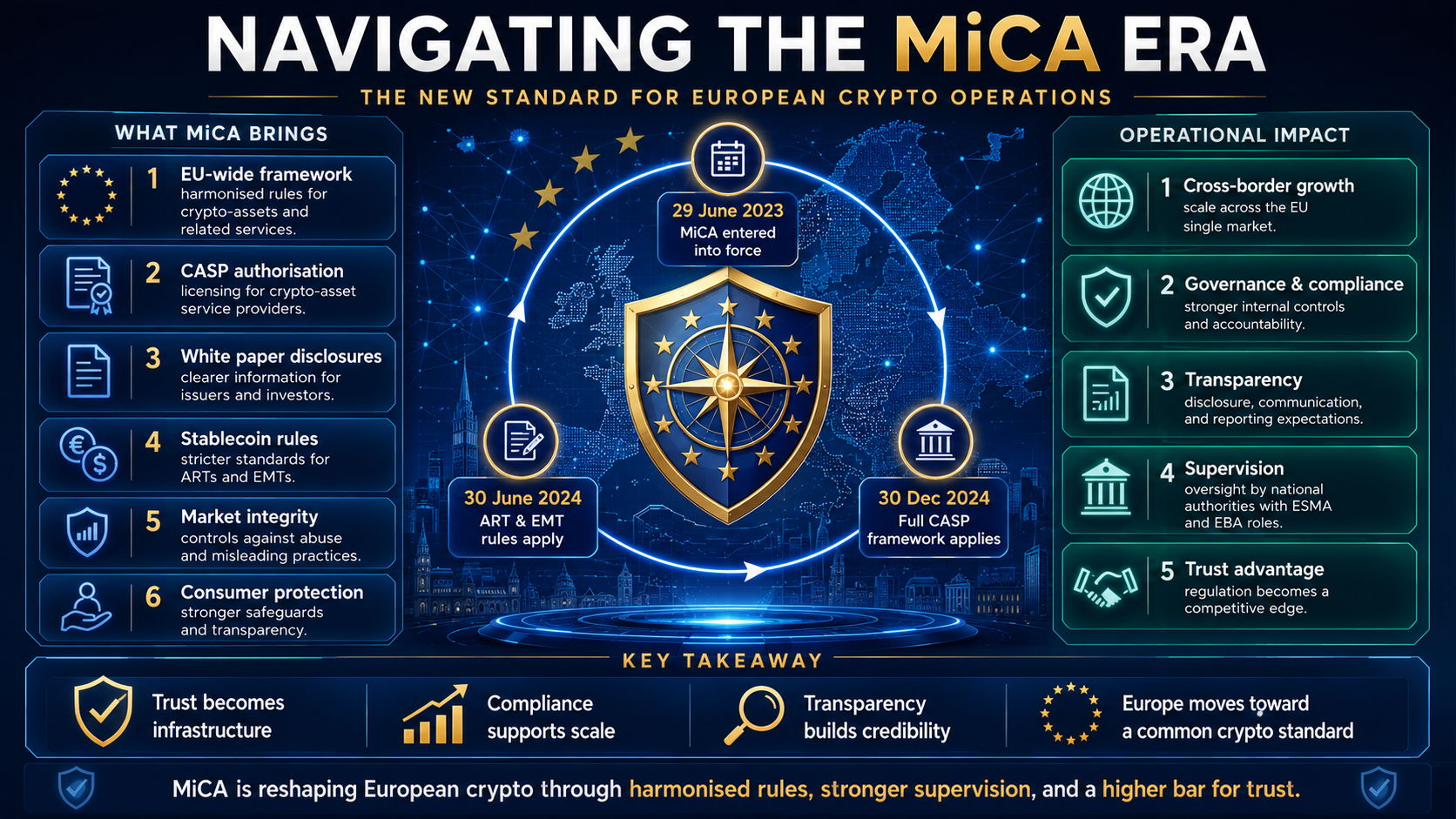

MiCA provides a comprehensive legal framework that harmonizes crypto-asset regulations across all European Union member states. By establishing clear requirements for consumer protection, market integrity, and financial stability, MiCA effectively replaces the patchwork of national laws with a single “passportable” license. This allows businesses to operate seamlessly across the entire EEA once they secure approval from a single national regulator.

For companies, this regulatory clarity is a double-edged sword. It requires rigorous compliance, internal audits, and stringent operational transparency. However, it also offers a significant competitive advantage: institutional legitimacy. In the coming years, we anticipate that businesses lacking a CASP license will face increasing barriers to entry, particularly as banking partners and institutional clients move exclusively toward regulated counterparties. Industry projections suggest that over 80% of major crypto firms will seek full MiCA compliance by the end of 2027 to remain viable in the European market.

“MiCA is not just a set of rules; it is the infrastructure for institutional adoption. It provides the legal certainty that has been missing, allowing legitimate players to scale with confidence.” — European Regulatory Counsel

Why is the Triple-A approval a significant benchmark?

The approval of Triple-A signals that regulators are increasingly comfortable with and ready to integrate global fintech innovators into the European fold. By proving their compliance with the robust standards set by French authorities, Triple-A has demonstrated that being “based in Singapore” does not preclude a firm from meeting the high-bar security and liquidity mandates of the EU.

This case serves as a roadmap for other non-EU fintechs. It proves that the “passporting” mechanism—the core benefit of MiCA—is functioning exactly as intended. A single license granted in France acts as an entry key to 30 national markets, drastically reducing the cost and complexity of scaling a crypto-asset business in Europe. This will likely trigger a wave of applications from high-quality international firms eager to capture the European user base without navigating 30 different legal systems.

How does MiCA impact retail consumers and institutional safety?

MiCA shifts the burden of trust from the user to the provider, mandating clear disclosures and liability for asset custody. Retail consumers are now protected by rules requiring providers to hold enough capital, secure their digital assets against hacks, and maintain transparent fee structures. Institutional investors, meanwhile, gain the regulatory cover they need to commit significant capital to digital assets, as they can now interact with providers that are legally bound to follow EU-standard governance.

The long-term impact on market safety cannot be overstated. By enforcing strict operational transparency, MiCA reduces the probability of catastrophic failures similar to those seen in the last market cycle. As compliance becomes the “price of admission,” the market is expected to mature, shedding bad actors and consolidating influence among firms that treat regulatory adherence as a core component of their business strategy.

What are the primary compliance pillars under MiCA?

The primary compliance pillars under MiCA include asset custody standards, stablecoin reserves, and rigorous anti-money laundering (AML) controls. Providers must prove they have the capital reserves to back their commitments, especially regarding stablecoins, and must provide detailed white papers for every asset they offer. Failure to meet these criteria results in immediate exclusion from the passporting benefits, effectively locking the company out of the EEA.

Furthermore, providers are now responsible for the environmental impact of the assets they support, with requirements to disclose the energy consumption of the underlying consensus mechanisms. This multi-layered compliance requirement ensures that only firms with mature operational structures can survive the transition.

How do you assess if a platform is MiCA-compliant?

To assess if a platform is MiCA-compliant, you should check for the official CASP status issued by a national regulator and verify their regulatory registration in the EU’s public databases. If a platform is operating in the EEA but does not explicitly hold an authorization from a member state regulator, it is likely non-compliant and carries significant risk for the user.

Professional users should look for clear evidence of independent audits, detailed disclosures of asset custody arrangements, and publicly listed information regarding their legal entity status within the EU. In the post-MiCA environment, a lack of clear regulatory documentation is no longer a sign of “crypto-native flexibility”—it is a red flag indicating a lack of institutional-grade governance.

What is the strategic future for crypto firms in the EU?

The strategic future for crypto firms in the EU is centered on “Regulatory Scalability.” The era of “move fast and break things” is over; the era of “move steadily and build trust” has begun. Firms that successfully integrate MiCA compliance into their product development cycle will be the ones that win the institutional race. By focusing on compliant infrastructure, these firms can unlock banking partnerships, institutional liquidity, and deeper retail trust.

As we look toward 2027, the gap between regulated entities and the “grey market” will widen substantially. We expect to see a surge in M&A activity, as larger, compliant firms acquire smaller, niche players to bolster their technological capabilities while leveraging their existing CASP licenses. For those currently planning their expansion, the message is clear: prioritize regulatory readiness as a primary product feature. The ability to operate as a regulated counterparty is not just a legal requirement—it is the ultimate competitive advantage in a maturing digital financial system. The winners of this phase will be those who view regulation as a catalyst for growth rather than a constraint on innovation.